Comparison Between the Old and the Updated Version of Egyptian Auditing Standard No. (200)

The Egyptian Auditing Standard No. (200) represents the cornerstone of the auditing profession, as it establishes the philosophical and professional framework that defines the nature of the auditor’s work, objectives, and responsibilities. With the update of Egyptian auditing standards to align with the International Standards on Auditing (ISA), this standard has undergone a fundamental transformation reflecting the evolution of professional thinking and the expansion of auditors’ responsibilities.

![]() Amer Ibrahim - • External audit and audit

Amer Ibrahim - • External audit and audit

The Egyptian Auditing Standard No. (200) represents the cornerstone of the auditing profession, as it establishes the philosophical and professional framework that defines the nature of the auditor’s work, objectives, and responsibilities. With the update of Egyptian auditing standards to align with the International Standards on Auditing (ISA), this standard has undergone a fundamental transformation reflecting the evolution of professional thinking and the expansion of auditors’ responsibilities.

Similarities Between the Old and the Updated Version

CopyDespite the update, the core principles of the standard have remained unchanged, continuing to emphasize:

- The overall objective of the external auditor: to express an independent opinion on the financial statements.

- The concept of reasonable assurance: the auditor provides reasonable assurance, not absolute assurance.

- Reliance on professional judgment and expertise.

- Commitment to independence and objectivity as fundamental pillars of the auditing profession.

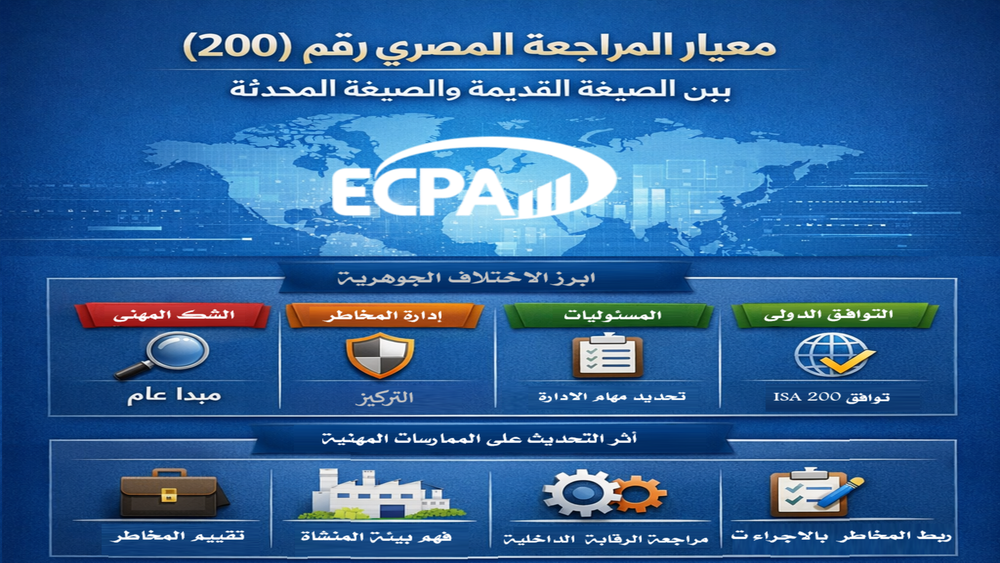

Key Fundamental Differences

Copy1. Strengthening Professional Skepticism

CopyOld version: referred to it as a general principle

.Updated version: treats it as a continuous mindset and a primary tool for detecting errors and fraud.

2. Focus on Risk Management

Old version: addressed risks implicitly.

Updated version: establishes a direct link with the Risk-Based Audit model.

3. Clarifying the Responsibilities of Management and the Auditor

Old version: maintained a traditional separation.

Updated version: provides a clearer and more detailed formulation, emphasizing that:

- management is responsible for preparing the financial statements and maintaining internal contro

- he auditor’s role is limited to expressing an independent opinion.

4. Strengthening Ethical Commitment

Copy- Old version: focused on general principles

- Updated version: directly linked to international codes of ethics, highlighting integrity, confidentiality, and independence of mind

5. International Alignment

CopyOld version: partial alignment

Updated version: almost full adoption of ISA 200.

6. Clarifying the Inherent Limitations of Auditing

CopyThe updated version provides more detailed explanations regarding:

- The use of sampling technique

- The possibility of collusion.

- Reliance on persuasive rather than conclusive audit evidence.

Impact of the Update on Professional Practice

CopyThe update has shifted the auditor’s role from a traditional examiner to a strategic auditor based on risk assessment and understanding the entity’s environment. Auditors are now expected to:

- Understand the business model of the entity.

- Analyze the economic environmen

- Evaluate internal control systems

- . Link identified risks with appropriate audit procedures.

Professional Importance of Standard 200 After the Update

CopyRepresents the philosophical foundation of the auditing profession

Serves as a reference point for other auditing standards

- Defines the nature of the audit process and the limits of the auditor’s responsibility

Enhances the quality of financial reporting and increases users’ confidence in financial statements.

Enhances the quality of financial reporting and increases users’ confidence in financial statements.

Conclusion

CopyThe update of Egyptian Auditing Standard No. (200) represents a qualitative shift in professional thinking. It reflects the global trend toward risk-based auditing, enhances the quality of professional practice, and places auditors before deeper and clearer responsibilities. It is not merely a formal update, but rather a redefinition of the auditor’s role in line with the requirements of the modern business environment.