Penalties that an auditor may be subjected to

The auditor represents an important role in controlling the work of financial management in joint stock companies and in view of the original right of shareholders to carry out this task and the difficulty in practice, the legislator has created a system of control over accounts

![]() Amer Ibrahim - • External audit and audit

Amer Ibrahim - • External audit and audit

Penalties that an auditor may be subjected to

The auditor represents an important role in controlling the work of financial management in joint stock companies and due to the original right of shareholders to carry out this task and the difficulty in practice, the legislator created the audit system for the first time by Law No. 26 of 1954 and regulated by the role of the auditor in Articles (51-54) of the law and the deficiency in this legislation was addressed in the Law No. 159 of 1981 Articles No. ( 103-109 ).

According to the first paragraph of Article 103 of Law 159 of 1981 (the joint stock company shall have one or more auditors who meet the conditions stipulated in the Law of Practicing the Accounting and Auditing Profession, appointed by the General Assembly and estimated his fees, and in the case of multiple auditors, they shall be jointly liable, and as an exception to that, the founders of the company shall appoint the first controller)

(First) the responsibility of auditors in accordance with Egyptian laws

The auditor is defined as the person entrusted by the group of partners to carry out internal control work such as reviewing and examining the company's accounts, budget, profit and loss accounts, the work of the board of directors and the extent of respect for the law in all of this and in a way that achieves the interest of the company, partners and the public interest.... He is also the person who performs the audit process, i.e. examining the internal control systems, data, documents, accounts and books of the company in an organized critical examination (through the analysis of accounts and the work of comparisons due to the detection of unusual matters) with the intention of coming up with an impartial opinion about the extent to which the financial statements indicate the financial position of the company at the end of a known period of time that depicts the results of its business of profit or loss for that period.

Article 104 of Law 159 of 1981 stipulates that " it is not permissible to combine the work of the controller with participation in the establishment of the company or membership of its board of directors or to work in a permanent capacity in any technical, administrative or consulting work therein, and it is also not permissible for the observer to be a partner of any person who carries out an activity stipulated in the preceding paragraph or to be an employee of me or from Zoe relatives up to the fourth degree."

This profession is practiced in the personal capacity of the observer and is prohibited from using in the practice of the profession the name of a legal person or an office or an accounting institution at the first audit.... The auditor performs his legal and contractual duties for a specific period of time stipulated in his appointment contract in return for fees estimated by the General Assembly of Shareholders.

The auditors of companies listed on the Egyptian Stock Exchange are required to be registered in the records of the Financial Supervisory Authority at the Quality Control Unit of the auditors' work registered in the records of the Financial Supervisory Authority.

Where the Financial Supervisory Authority has established a special register for the registration of auditors who may review companies whose papers are listed in securities exchanges, public placement companies operating in the field of securities and investment funds established in banks and insurance companies under the decision of the Board of Directors of the Authority No. 33 of 2009 issued on April 29, 2009, in which several conditions were stipulated for registration clarified by the aforementioned law.

The general assembly of the company is the owner of the original competence in appointing the auditor, determining the fiscal year to which he is delegated and determining fees.

(Second) The role of auditors in verifying the validity of financial statements and reports

The auditors' reports on the financial statements of companies is the main and most important role in the auditor's responsibilities towards the general assembly of the company because the financial statements are the ones that reflect the success or failure of the elected board of directors in carrying out its responsibilities in managing the company's shareholders' funds... The auditor shall exert professional care to reach a fair and clear opinion on the correctness of the statements and balances in the financial statements during a specific period of time... The auditor has several rights and duties, which are summarized as follows:

1. The rights of the auditor as an external supervisory body

1 - The right to fully access all the books and records of the company, whether accounting or non-accounting, whether mandatory or optional - and if he is unable to exercise this right, he must submit a report on this matter to the Board of Directors and present it to the General Assembly of Shareholders and there is no responsibility on the auditor if he is unable to view the documents that enable him to develop his report freely and independently.

2 - The right to request additional data and analysis necessary to form an opinion on the financial statements.

3 - The right to obtain a copy of the notifications sent to shareholders.

4 - Invite the General Assembly of Shareholders to convene if he deems that there are emergency circumstances that must be presented to the General Assembly.

5 - The right to defend himself and discuss the proposal of his dismissal or dismissal.

6 - The right to withhold the documents and papers of the customer until he gets his fees.

2. Duties of the auditor as an external regulator

1 - General control of accounts through the process of reviewing the accounting data recorded in the company's records to obtain a clear neutral opinion on the company's financial statements.

2 - Submit an annual report to the General Assembly on the validity and fairness of the company's financial statements.

3 - Verification of equality between shareholders.

4 - Attending the General Assembly of Shareholders and monitoring the validity of its convening.

5 - Prohibition of business work.

6 - Maintaining the secrets of the company.

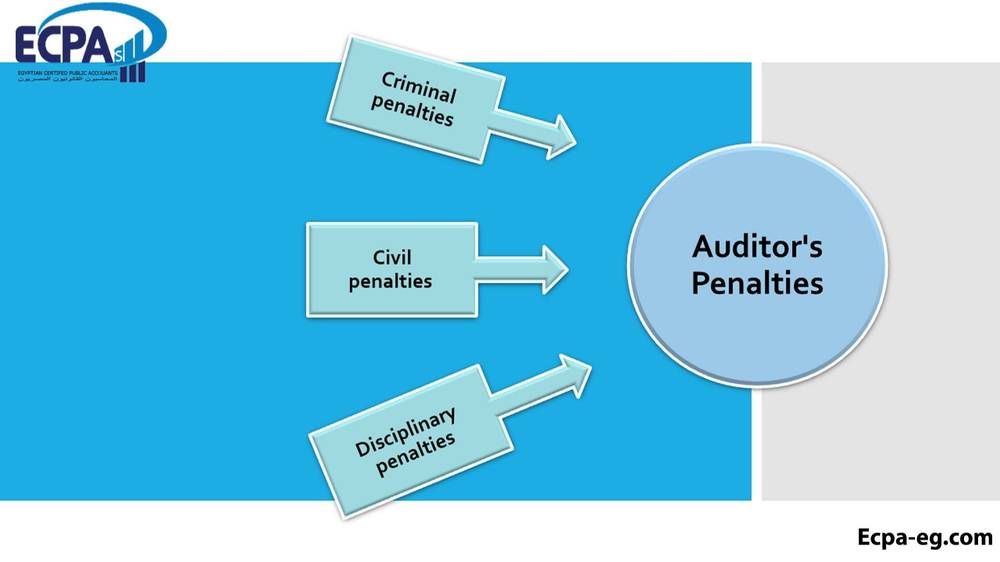

(III) Penalties and liabilities to which auditors may be exposed.

Through the above - and in light of the rights and encounters that the auditor specialized, it is clear the importance and seriousness of his commitment to express an impartial and fair opinion on the validity of the company's financial statements by taking into account the exercise of professional due diligence to reach this technical opinion stemming from the independence and impartiality granted to him by the standards and laws.

And here comes the question ... What are the penalties that the auditor may be exposed to in case of breach or default of his duties and responsibilities???

The answer to this question is summarized in the fact that the auditor is subject to penalties that vary in nature according to the type of error made by the auditor. It is limited to:

1. Disciplinary sanctions

It is related to the extent of its commitment to professional behavior and breach of the duties of practicing the profession - and disciplinary penalties are:

1. Prognosis

2. Reprimand

3. Deprivation from practicing the profession for a period not exceeding two years

4. Removal from the register of accountants and auditors

The disciplinary trial shall be at the headquarters of the Association and in a secret session, and he shall have the right to appeal the decision issued and submit documents indicating his innocence.

5. Civil penalties (civil liability)

It is divided into:....

1. Contractual liability

It is related to the auditor's breach of the terms of the contract concluded with the client (the company) - and the client has the right, in the event of damage as a result of this default or breach, to claim the auditor for appropriate compensation for this damage.

2. Tort Liability

It is that damage falls on any other parties (other than the company's shareholders) because of the auditor's negligence in his duties - and although these parties are not an original party in the contract with the auditor, but his responsibility arises from the impact of damage to the users of the financial statements, which was issued a report on them contrary to their truth as a result of negligence or collusion and here comes the role of the judiciary in adjudicating in such cases to determine the availability of the conditions for deliberate failure to express a sound opinion about Financial statements – until the appropriate judgment is issued on a case-by-case basis.

3. Criminal penalties (criminal liability)

It is related to the auditor committing a mistake up to the degree of crime stipulated by law, such as... Forgery, fraud, or breach of trust. These are crimes to which the Penal Code applies.

The auditor shall be punished by imprisonment or a fine or both in accordance with the Egyptian laws regulating these crimes.